Leverage, panic and mind traps: Navigating uncertainties

Here's all that Mint Money covered this week.

The markets are all anyone seems to be talking about these days, given the volatile swings and drawdowns in the wake of the Iran war with the US and Israel. Although the temporary halt to strikes announced by the US did help markets recover to some extent, it’s clear we haven’t heard the end of it yet.

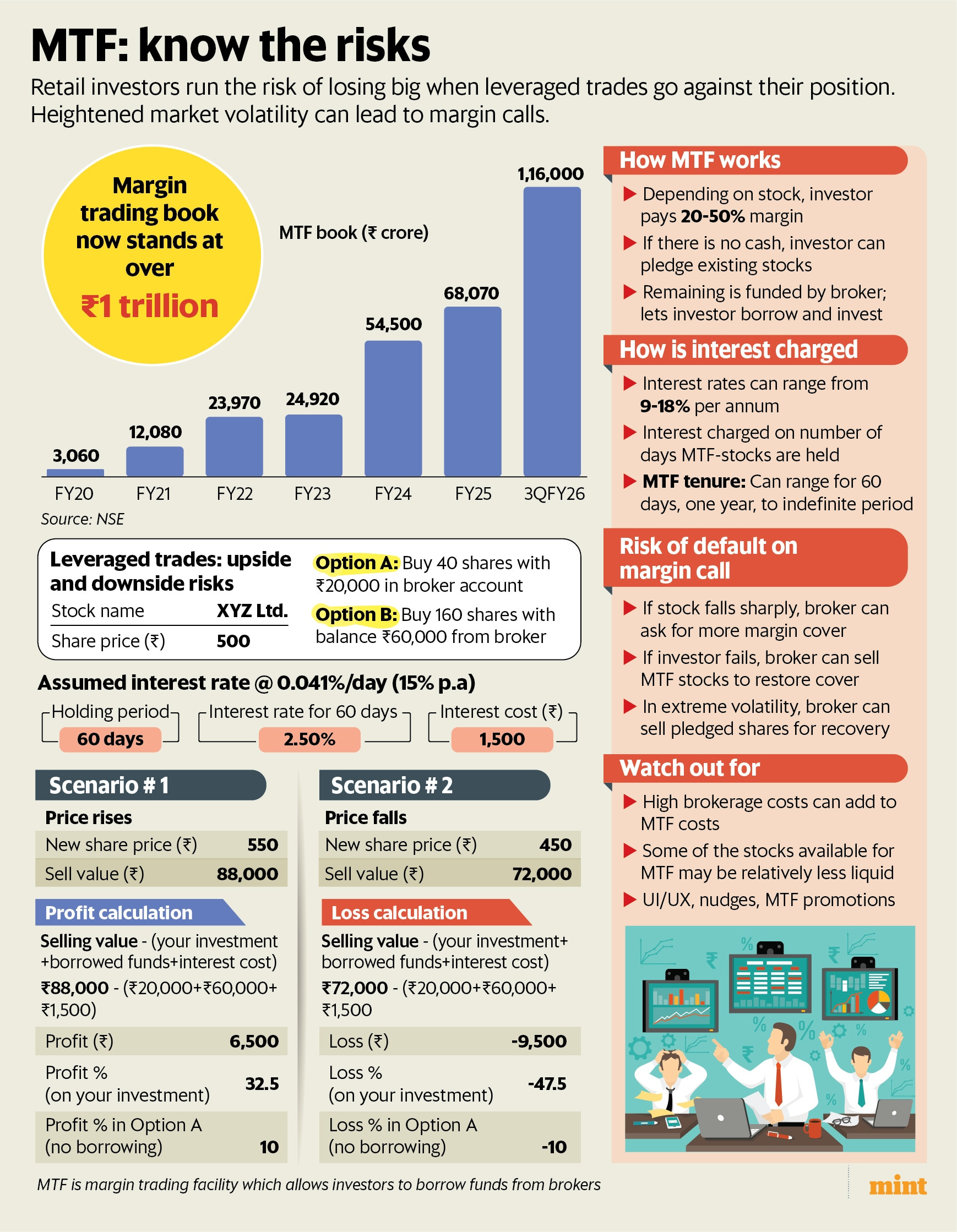

The nervous energy in the market isn’t just about fundamentals, it’s being amplified by leveraged retail traders. India’s margin trading market has hit ₹1 trillion, reflecting how tempting leverage can be: invest a small amount, borrow the rest, and take bigger bets on stocks you believe in. The growing pool of margin trades also means that reactions to volatility—often hasty and panic-driven—tend to amplify price swings.

This is why trades funded by borrowed money carry serious, potentially fatal risks. Gains can rise sharply when trades work out, but losses can spiral much faster due to leverage and associated costs. Jash Kriplani, in this excellent story, walks you through the hard math of how margin trading can boost gains, but make losses far worse.

Once you distill this to understand why margin trading isn’t for everyone, especially as a tool for building long-term wealth, there is another insightful piece by Dhirendra Kumar. In his weekly column, Kumar explains exactly how market volatility gets amplified by the behaviour of leveraged investors. Borrowed money isn’t patient, it comes with pressure and urgency. As he writes, when you borrow to invest in stocks or take positions in futures and options, you are no longer deploying patient capital. You are using money that charges a daily rent and can be forcibly withdrawn if prices move against you.

So when prices fall, these investors are often forced to exit quickly, intensifying volatility. But that panic isn’t yours to own, Kumar reminds long-term investors; it belongs to those operating under leverage.

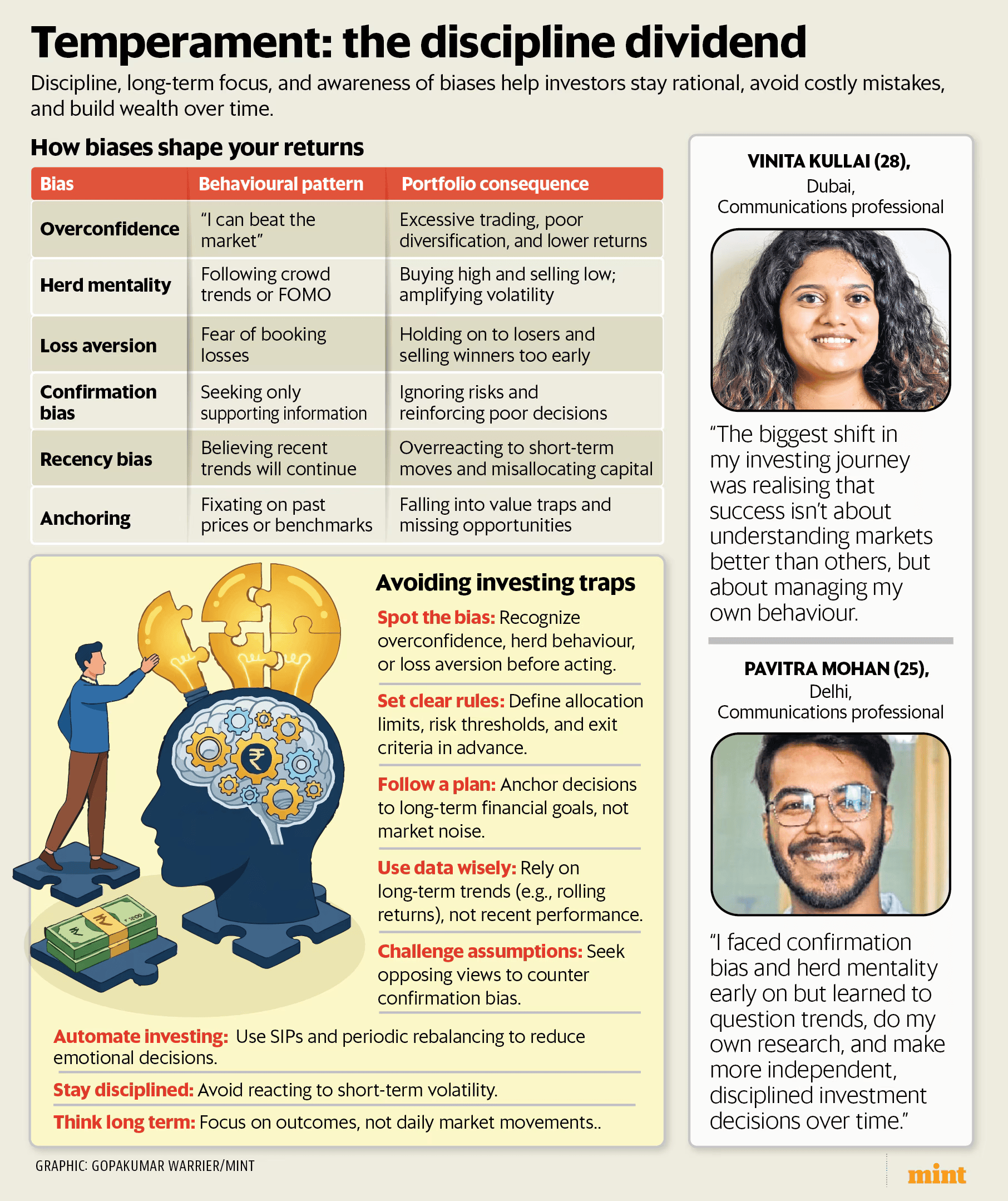

But it’s not just panic that investors need to guard against, behavioural traps of the mind can be equally overpowering in volatile and uncertain times. Anagh Pal takes you through key behavioural biases: recency bias, where investors take a myopic view based on recent experience; herd mentality, which draws comfort from following the crowd; overconfidence in one’s own judgement, and confirmation bias, which seeks out information that validates existing beliefs.

Together, these biases can push investors into poor decisions like buying high, selling low, panicking during volatility or chasing hot asset classes. Discipline and emotional control matter just as much as intelligence or market knowledge in generating long-term returns. Many investors underperform not because of bad investments, but because of how they react to volatility. Managing one’s emotions, therefore, is as critical as managing one’s portfolio.

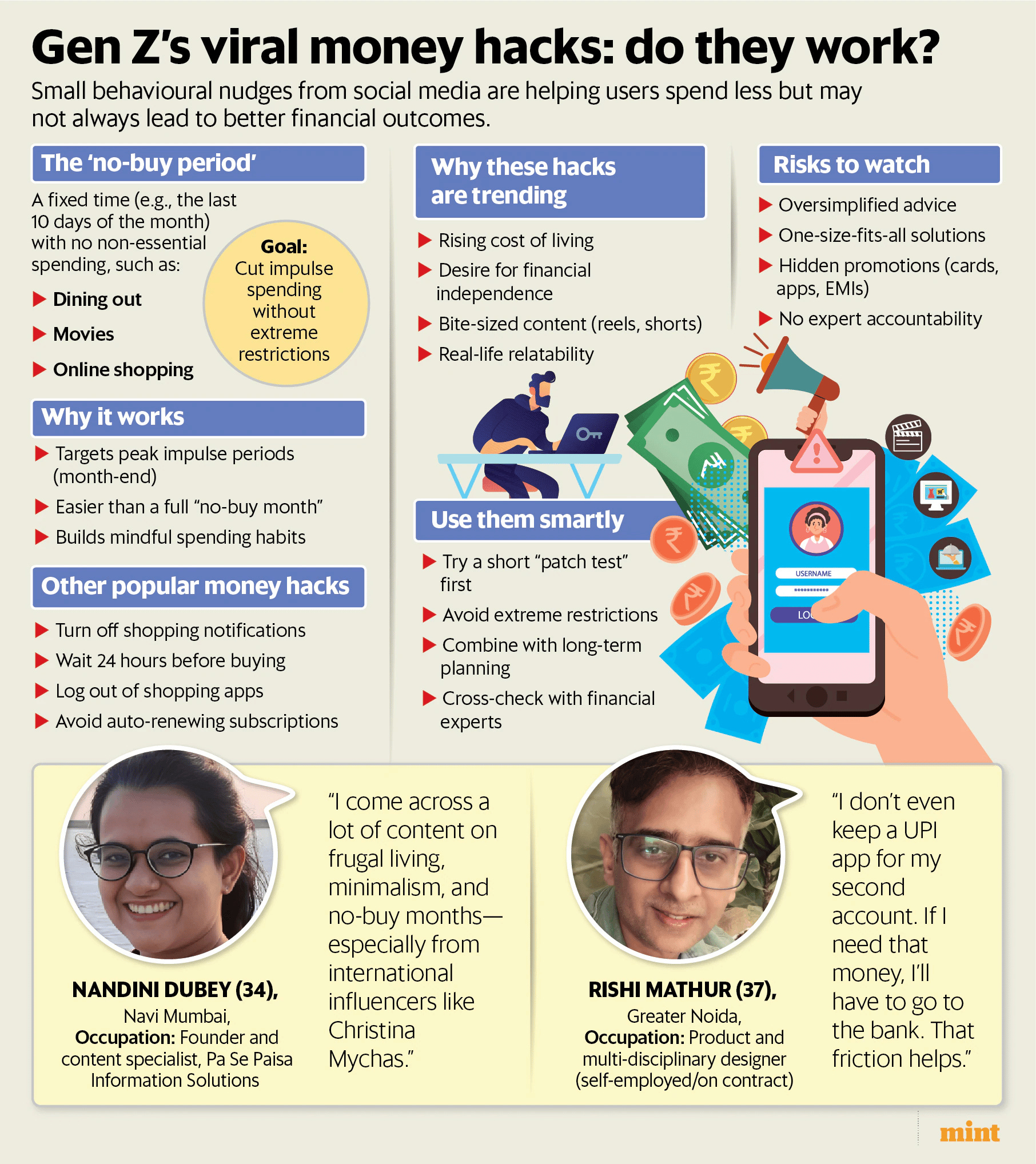

And to influence your behaviour you also have social media noise on money management. Social media is full of tips and hacks to help you become more disciplined with your money. Trends like “no-buy days” and 24-hour cart pauses aim to curb impulsive spending, making financial discipline feel more accessible and relatable especially for the younger lot by encouraging small, manageable changes. Rising living costs and economic uncertainty are also driving this shift.

However, such oversimplification can be misleading. Personal finance is deeply individual and broad rules without context need to be approached with caution. A no-buy challenge, for instance, may curb spending for some but trigger binge spending later for others. It’s also worth noting that when influencers promote such hacks, they may carry hidden incentives.

Ultimately, while these habits can be a useful starting point, what’s needed is a more comprehensive and personalised approach, writes Ann Jacob in this story.

For first-time earners moving to metros and experiencing financial independence with their paycheques, this timely story by Ananya Grover highlights a growing concern. Rent now consumes a significant share of income, making the traditional advice of keeping it under 30% of take-home pay increasingly irrelevant. Consider this: the average monthly net salary in Mumbai is about Rs 70,551, while a one-bedroom apartment in the city centre costs around Rs 60,533.

Clearly, rents are outpacing entry-level salaries and the trade-off is between convenience, comfort and savings. While affordability is subjective, excessive rent can delay financial stability by limiting early savings and the benefits of compounding. It’s therefore important to strike the right balance early on.

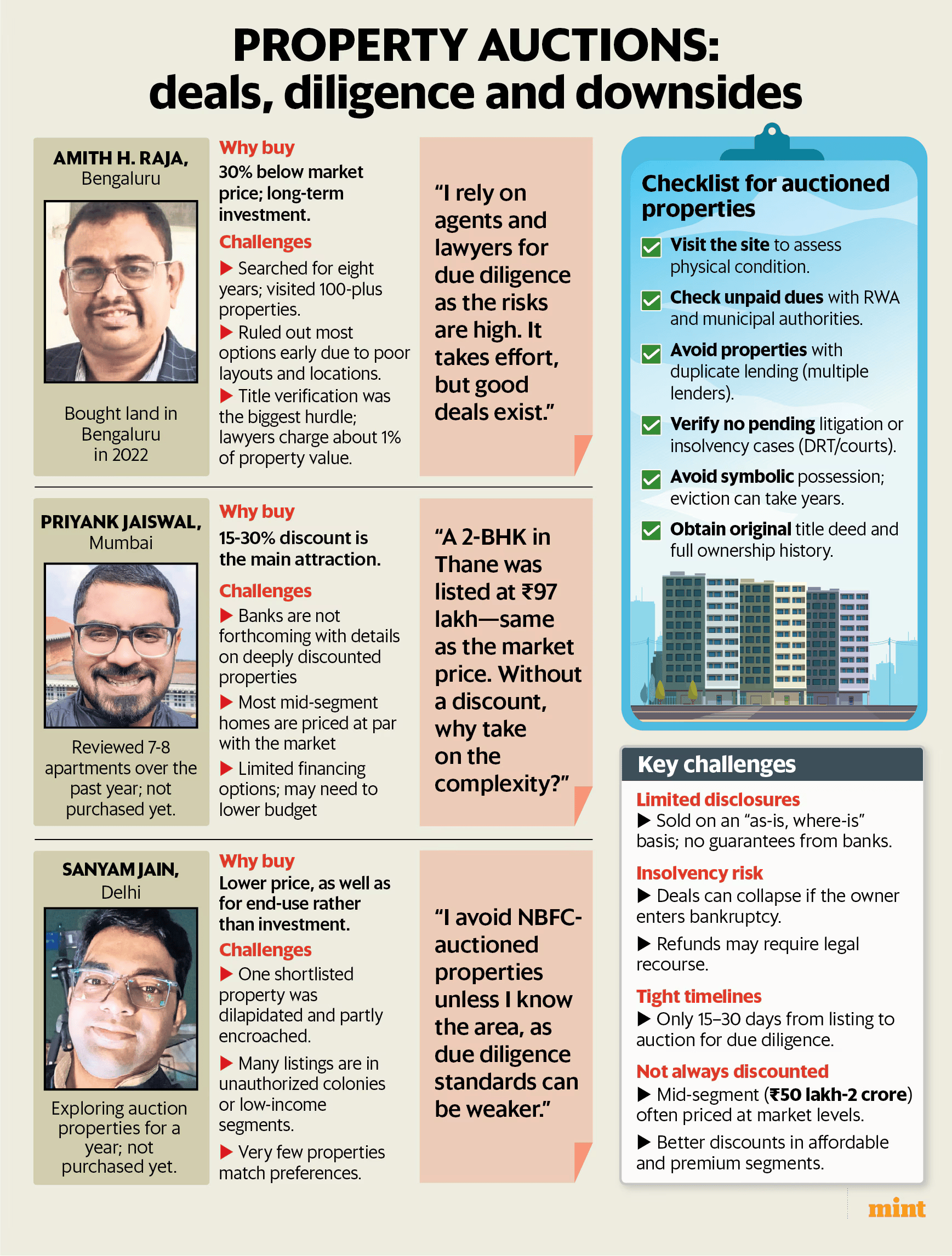

Shipra Singh brings a timely piece on auctioned properties. Auctioned properties often look like a steal on paper, with discounts that can go up to 30%. But that’s where the rosy narrative ends and the grey areas begin. From unclear property conditions and possible encroachment, specially if the property has been vacant, to complications like multiple lenders staking claims or pending dues, these risks can quickly erode the apparent discount and turn the purchase into a costly mistake. The story speaks to buyers who have either purchased or actively explored auctioned properties, distilling their experiences into a practical checklist of what to watch out for before getting carried away by the price cut.

And finally, watch this video featuring Nilesh Shah, group president and managing director of Kotak Mahindra Asset Management Company, who shares his perspective on managing money in an increasingly uncertain world. It’s a must-watch for practical financial tips that can help you stay afloat.

Jash Kriplani also speaks with Sahil Kapoor, head of products and markets strategy at DSP Mutual Fund, who explains why the firm has turned bullish on equities after months of maintaining a conservative stance, following the recent sharp market correction.

That’s all from the Mint Money team for this week. Until next time!

Deepti Bhaskaran is editor, Mint Money, with two decades of experience as a personal finance journalist. Her work reflects a strong focus on financial literacy, consumer protection and practical money management. She can found at deepti.bhaskaran@livemint.com.