The next chapter in retirement planning

India’s young demography may promise a significant economic dividend, but the absence of structured retirement planning poses an equally significant challenge.

There is a silent crisis brewing in Indian households—the retirement crisis. India’s young demography may promise a significant economic dividend, but the absence of structured retirement planning poses an equally significant challenge—one that most households will eventually have to confront.

It was with this objective that the National Pension System was envisioned. Designed as a retirement solution for India’s vast workforce employed in the informal sector or private jobs, NPS focused heavily on the accumulation phase. The de-accumulation phase—how retirees generate a steady income after retirement—was largely left to annuities.

Under the original NPS structure, subscribers could build a retirement corpus through asset allocation strategies until the age of 60. At retirement, they were mandatorily required to annuitise 40% of the corpus. In effect, a substantial portion of retirement savings had to be locked into an annuity at prevailing rates. The remaining 60% could be withdrawn tax-free and used at the subscriber’s discretion.

But the focus remained on building a retirement corpus, not generating sustainable income after retirement. The NPS is no longer a nascent product. It is now reaching maturity, with a growing number of subscribers approaching retirement and looking for dependable income solutions.

Recognising this challenge, the pension regulator last year reduced the mandatory annuity threshold from 40% to 20%, giving retirees greater flexibility in accessing the corpus. But that solved only part of the problem. For financially unsavvy retirees, the question of how to manage the withdrawable corpus remained unresolved.

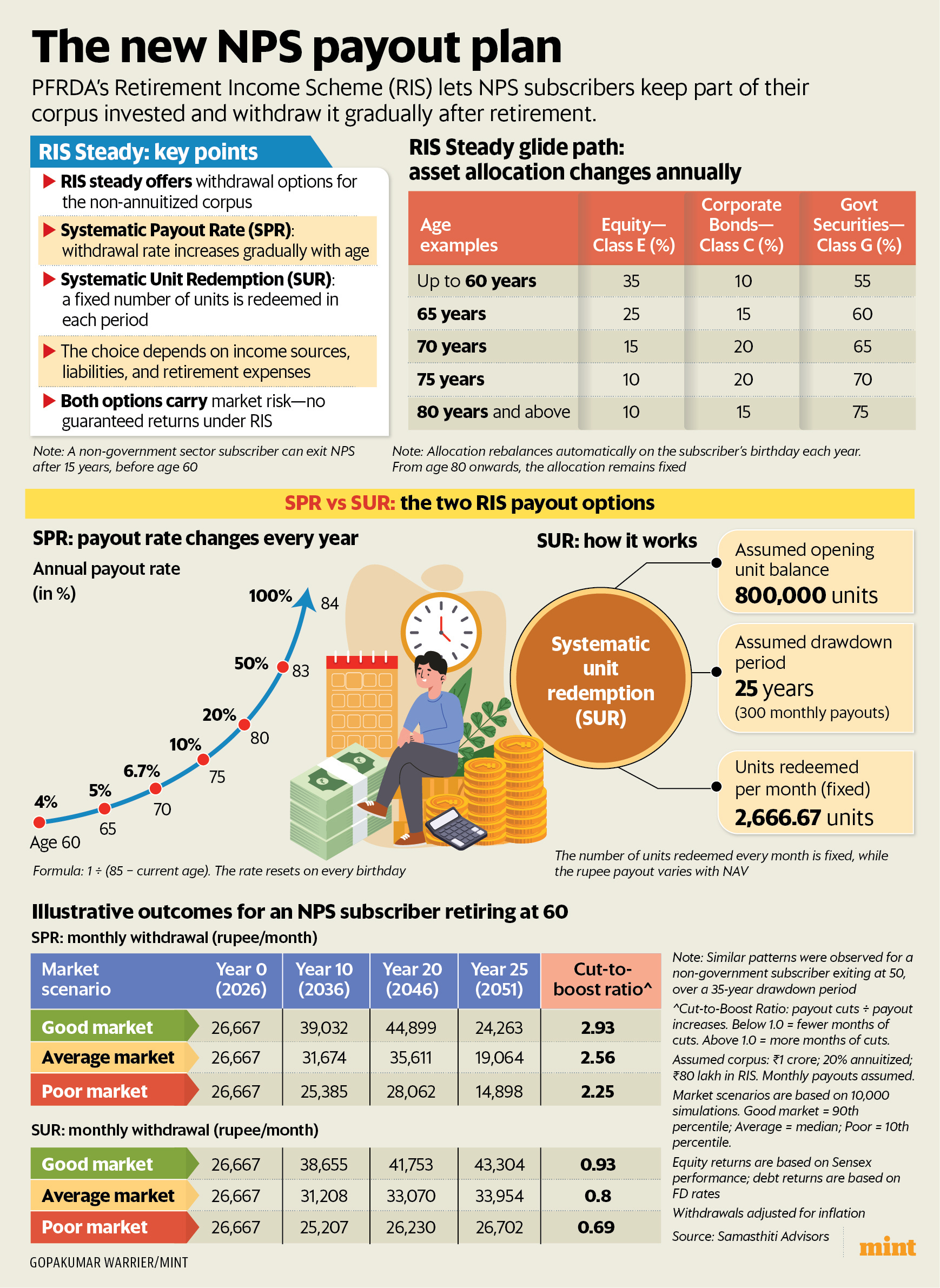

This year, the Pension Fund Regulatory and Development Authority attempted to address that gap with the introduction of the Retirement Income Scheme. Under RIS, subscribers at maturity will have two payout options extending up to the age of 85.

The first, called the Systematic Payout Rate, offers withdrawals at a pre-defined rate. The formula is simple: 1 divided by (85 minus the subscriber’s current age). For instance, at age 60, the withdrawal rate works out to roughly 4%, gradually increasing until the entire corpus is exhausted at 85. Since the corpus remains invested across equity, government securities and corporate bonds, only the withdrawal rate is fixed; the actual payout will still depend on the underlying fund value.

The second option, the Systematic Unit Redemption, works differently. The entire corpus is divided into equal units based on the withdrawal frequency chosen by the subscriber, and payouts depend on the value of those units at the time of redemption.

Jash Kriplani examines both approaches, analyses the kind of payouts investors can expect under different market conditions, and offers insights into which option may suit different kinds of retirees.

The second big story of the week is on insurance. For an insured patient, the process of cashless claim authorisation typically unfolds in two stages. The first occurs at the time of hospitalisation, when the hospital shares an initial report detailing diagnosis and proposed line of treatment with the insurer. Based on this, the insurer grants pre-authorisation for the cashless claim.

The second stage takes place at discharge, when the final set of medical documents and bills are submitted to the insurer for settlement approval before the patient can leave the hospital. To speed up this process and ensure that patients receive timely treatment without immediate out-of-pocket expenses, the IRDAI mandated a one-hour timeline for pre-authorisation approvals, the first leg of the claims process.

In theory, a pre-authorisation approval should lead to a smooth claims settlement process. Any subsequent disputes should ideally arise only if the treatment course changes significantly or new medical information comes to light.

But what is increasingly playing out is very different. Claims are being rejected at discharge on grounds such as non-disclosures or policy exclusions—issues that arguably should’ve been identified and addressed at pre-authorisation stage itself.

Aprajita Sharma spoke with policyholders to understand how quick pre-authorisation approvals later turned into distressing disputes and claim rejections. Their experience reveal how timelines may be followed in letter, but not always in spirit.

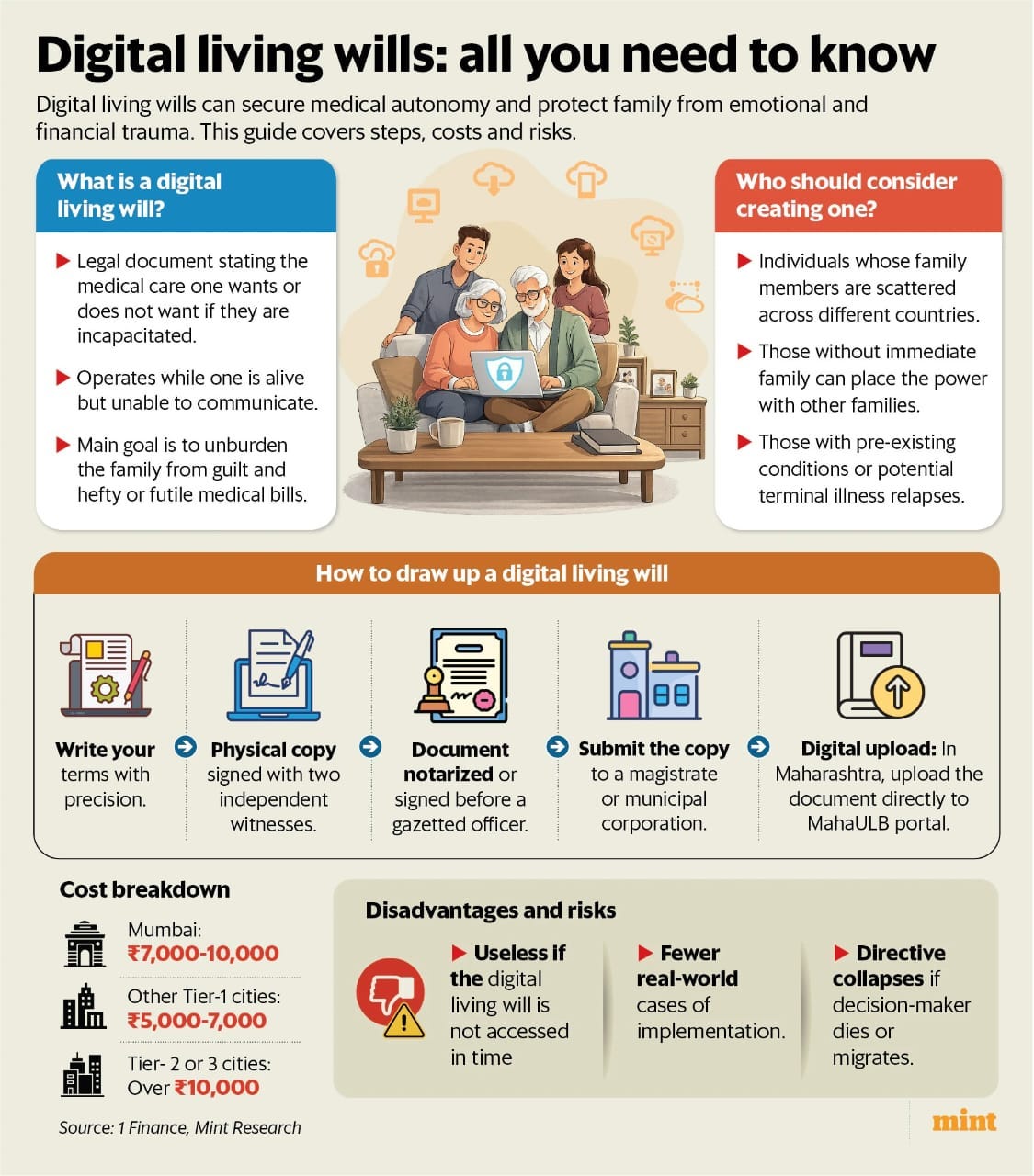

Ann Jacob this week writes about living wills, a concept becoming increasingly relevant in the context of changing family structures.

Imagine being critically ill and incapacitated, unable to make decisions about the course of medical treatment you would prefer. In such situations, the burden of decision-making falls on family members or relatives, often becoming a source of conflict, confusion and emotional strain.

Now imagine having a living will that clearly outlines your treatment preferences and designates who should make decisions on your behalf. The situation shifts from a high-stress dispute to a clearly defined plan of action focused on execution rather than disagreement.

Why is this becoming more important now? Because modern families function very differently. Family members may be dispersed across continents. Some individuals may have more than one family structure to navigate, while others may choose to remain single but rely on close friends or extended relatives for support. In all such cases, a living will can provide much-needed clarity and certainty.

Acknowledging the growing importance of living wills, Maharashtra has launched a dedicated module for digital living wills on the MahaULB portal. The story explains the mechanics, legal safeguards, costs and risks associated with digital living wills.

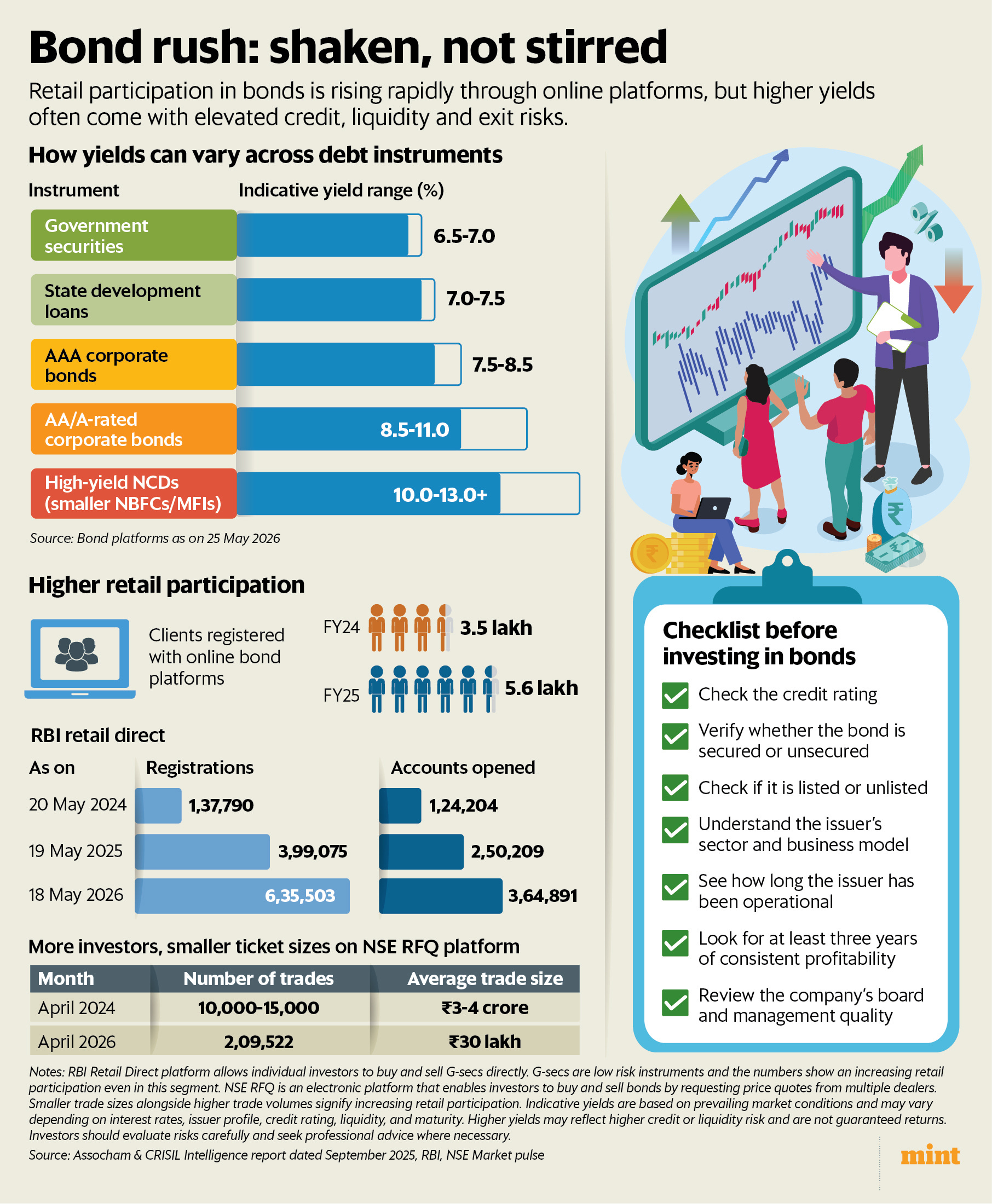

In the investment space, Ananya Grover writes about the dangers of approaching bonds with the risk appetite of fixed deposits.

Online bond platforms are increasingly showcasing corporate bonds and non-convertible debentures offering attractive yields. The temptation to move into debt products promising returns higher than fixed deposits is real—and many investors are taking the plunge.

A September 2025 report by Assocham and Crisil Intelligence highlighted this trend. The number of clients registered with Online Bond Platform Providers (OBPPs)—the SEBI-regulated platforms that allow retail investors to buy and sell listed bonds online—rose to 560,000 in FY25 from 350,000 in FY24. The monthly average retail trading volumes have also grown at a compounded annual growth rate of around 20% since OBPPs were introduced in 2022.

But while investors are chasing better returns, many fail to fully understand—or even account for—the risks these products carry, ranging from credit risk to liquidity risk. Higher yields often come with higher risk, a reality that can get overlooked in the rush for returns. The story details the essential checklist investors should keep in mind before buying bonds.

And finally, Shipra Singh writes about the second-order impact of a conflict raging in West Asia—one that has disrupted oil and gas supplies, pushed up fuel prices and weakened the rupee.

As fuel costs rise, logistics becomes more expensive, feeding inflationary pressures across the economy. The consequences are likely to be felt not just in higher day-to-day household expenses, but also in weaker earning potential for businesses, eventually weighing on household income growth.

Given this backdrop, the central bank—which until now has maintained a dovish stance and cut interest rates—is likely to shift to a neutral position and subsequently turn hawkish if current conditions persist.

Households, too, may need to take a cue from the central bank and reassess spending patterns. This is not a time for excessive optimism. Conserve financial resources and prioritise essential commitments such as tuition fees, insurance premiums, SIPs and EMIs, while postponing discretionary big-ticket purchases until the outlook becomes clearer.

In this week’s Money Guru, Ananya Grover spoke with Rishi Kohli, chief investment officer at Jio BlackRock AMC, who argues that fund managers need to move beyond pure stock selection for alpha and instead combine stocks, sectors and factor-investing strategies to generate excess returns for investors.

That’s all from the Mint Money team this week. Until next time!

Deepti Bhaskaran is editor, Mint Money, with two decades of experience as a personal finance journalist. Her work reflects a strong focus on financial literacy, consumer protection and practical money management. She can found at deepti.bhaskaran@livemint.com.