When the math stops working—from foreign degrees to fuel costs

As rupee weakens and costs rise, the economics of aspiration—from foreign education to everyday spending—is becoming harder to justify.

For as long as I can remember, studying abroad has been the ultimate middle-class aspiration in India. One of the earliest books that captured this obsession for me was Anurag Mathur's The Inscrutable Americans.

It follows the journey of a small-town boy who heads to the US for higher studies. Through his eyes and with a generous dose of humour the book explores India’s fascination with the West, the prestige attached to foreign education and the belief that better opportunities lie overseas. Decades later, that aspiration hasn’t faded. If anything, it has spread deeper into many more households. But what has changed significantly is the economic logic.

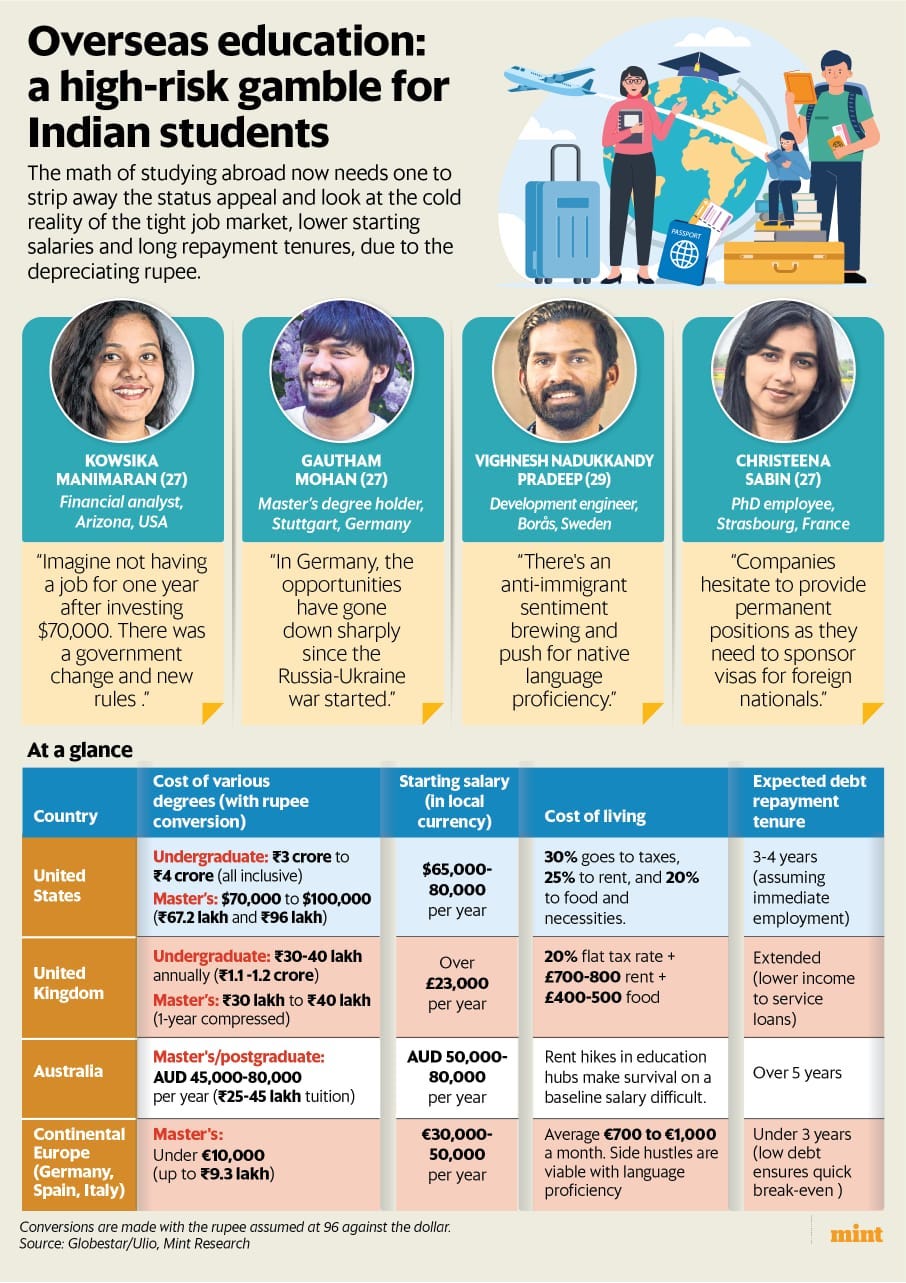

The global economy is more uncertain, job markets are tighter, and the rupee is falling, making the cost of studying abroad higher. A $70,000 course that would have cost about ₹59.5 lakh when the rupee was around ₹85 to a dollar about a year ago now costs more than ₹67 lakh, as the rupee has crossed ₹96 to a dollar.

Add to this the living expenses and the lack of job guarantees, and the math is painful. The assumption that a foreign degree quickly pays for itself is no longer a given. In this context, Ann Jacob’s story takes a closer look at the true cost of foreign education today. Through conversations with students across countries, it captures a growing reality—finding a job is no longer easy, and the financial payoff of an international degree is far less certain than it once was.

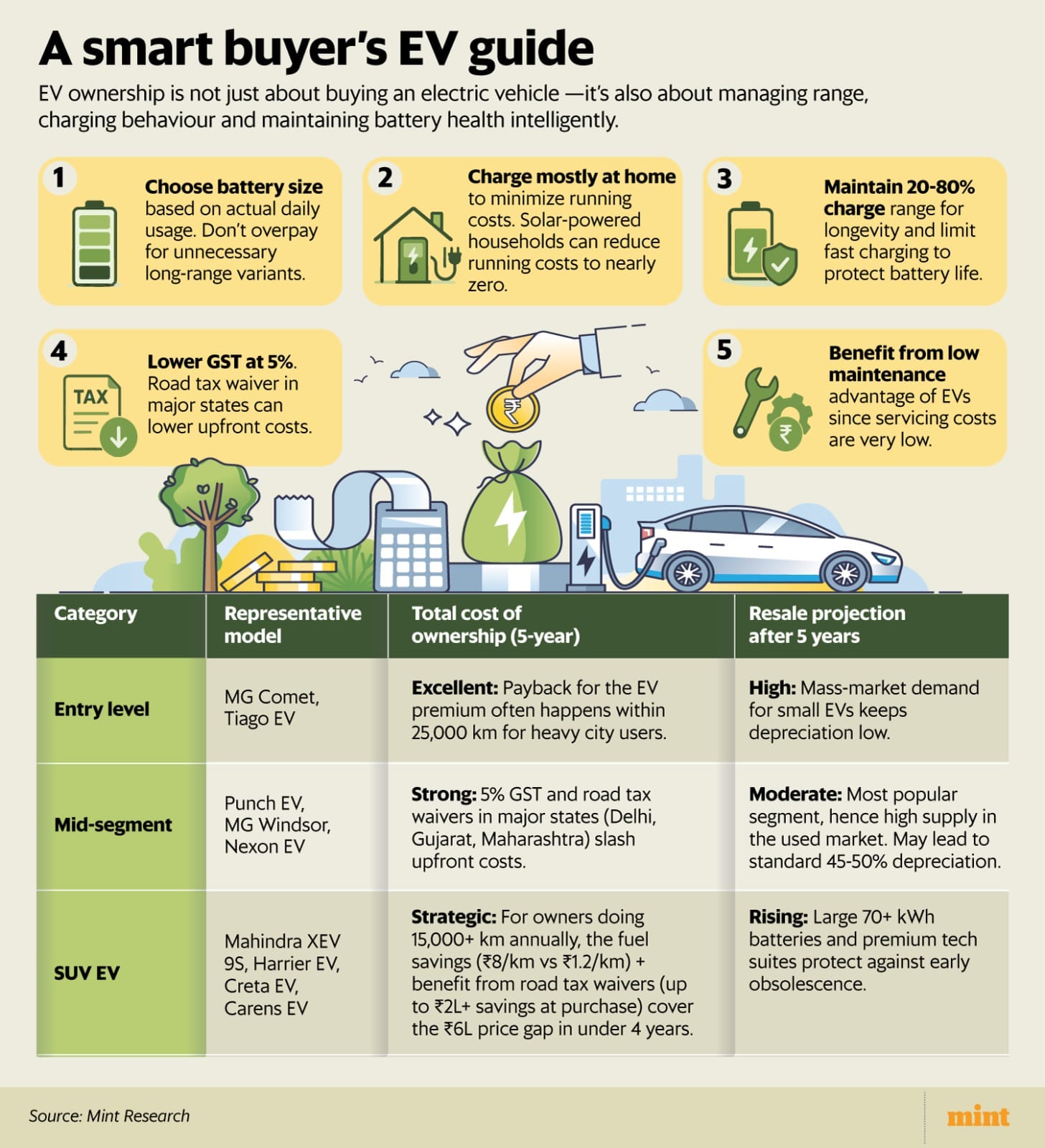

A weakening rupee, driven by geopolitical tensions in West Asia and foreign investor outflows, has begun to add to inflationary pressures, particularly through higher fuel costs. Fuel prices have risen recently, with many states seeing a hike of at least ₹3 per litre. With oil imports becoming more expensive, concerns around current account deficit and inflation are back in focus. In response, the government has signalled a need for austerity, with households also expected to play a role by curbing gold purchases, limiting foreign travel and reducing fuel consumption.

Against this backdrop, electric vehicles are getting a renewed economic push. Ashwin Moorthy takes this argument further, detailing how to extract maximum value for money from your EV. As it turns out, much of it comes down to how you use and maintain the vehicle.

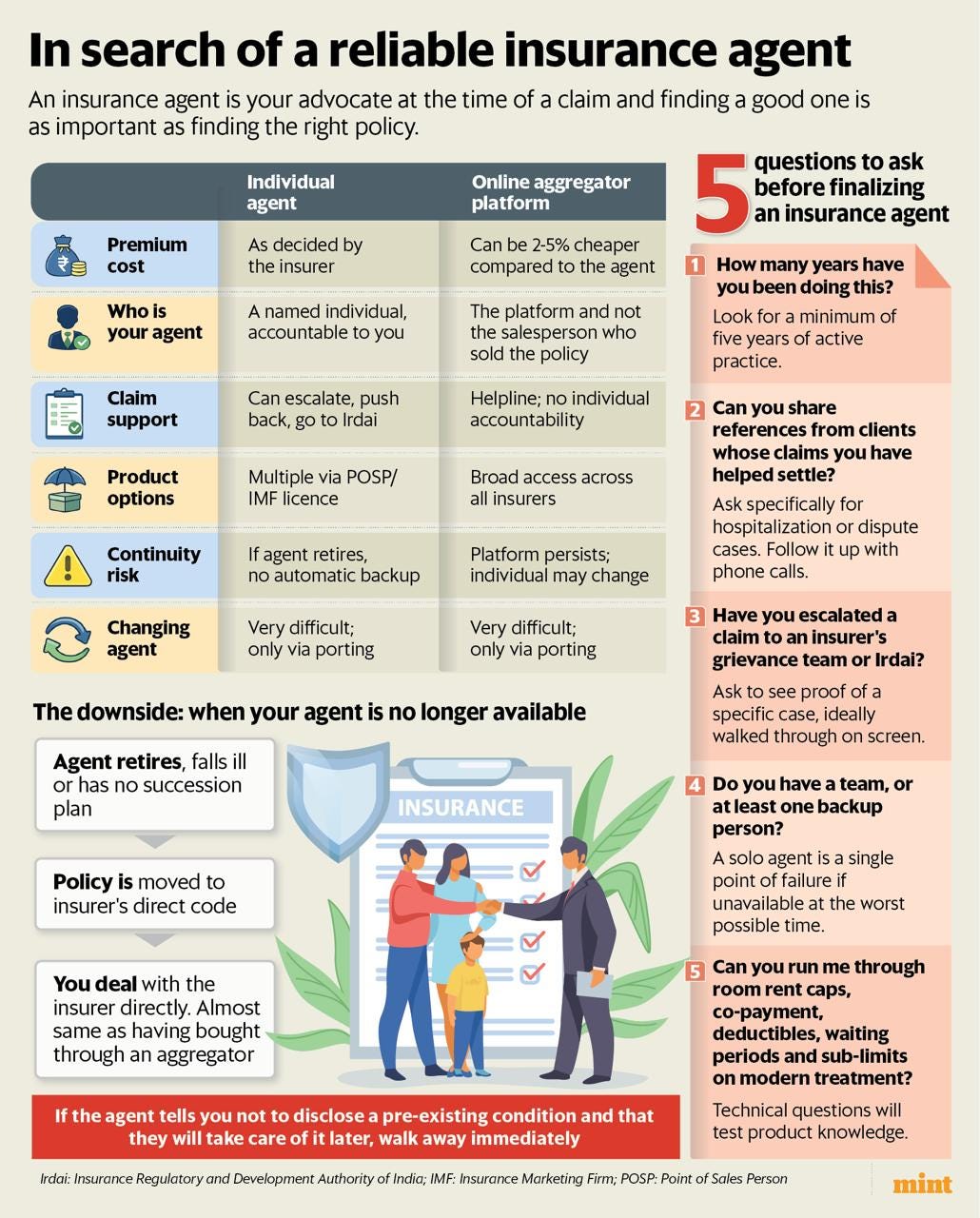

In the insurance space, Mint Money has two interesting stories. The first is the importance of having the right insurance agent by your side. Buying insurance is only half the job done, as how you buy dictates your experience during the moment of truth or when you make a claim. Because the real test of insurance comes at the time of claim, and that’s where things can fall apart.

Consider this: You purchase a health insurance policy through an agent who asks you to gloss over the proposal form and skip health disclosures to speed up the process. Later, you are hospitalised for something as routine as food poisoning, but the doctor notes that you are hypertensive—information you did not disclose at the time of purchase. That omission can give the insurer grounds to reject your claim. Just like that, your insurance becomes useless.

Insurance is built on the principle of utmost good faith, and it’s important your agent understands and respects this tenet. In this story, Shipra Singh outlines the checks and balances you should look for in an agent, so that you have a trusted aid who does not just sell you a policy, but ensures it stands up when you actually need it, and stays with you through the claims process.

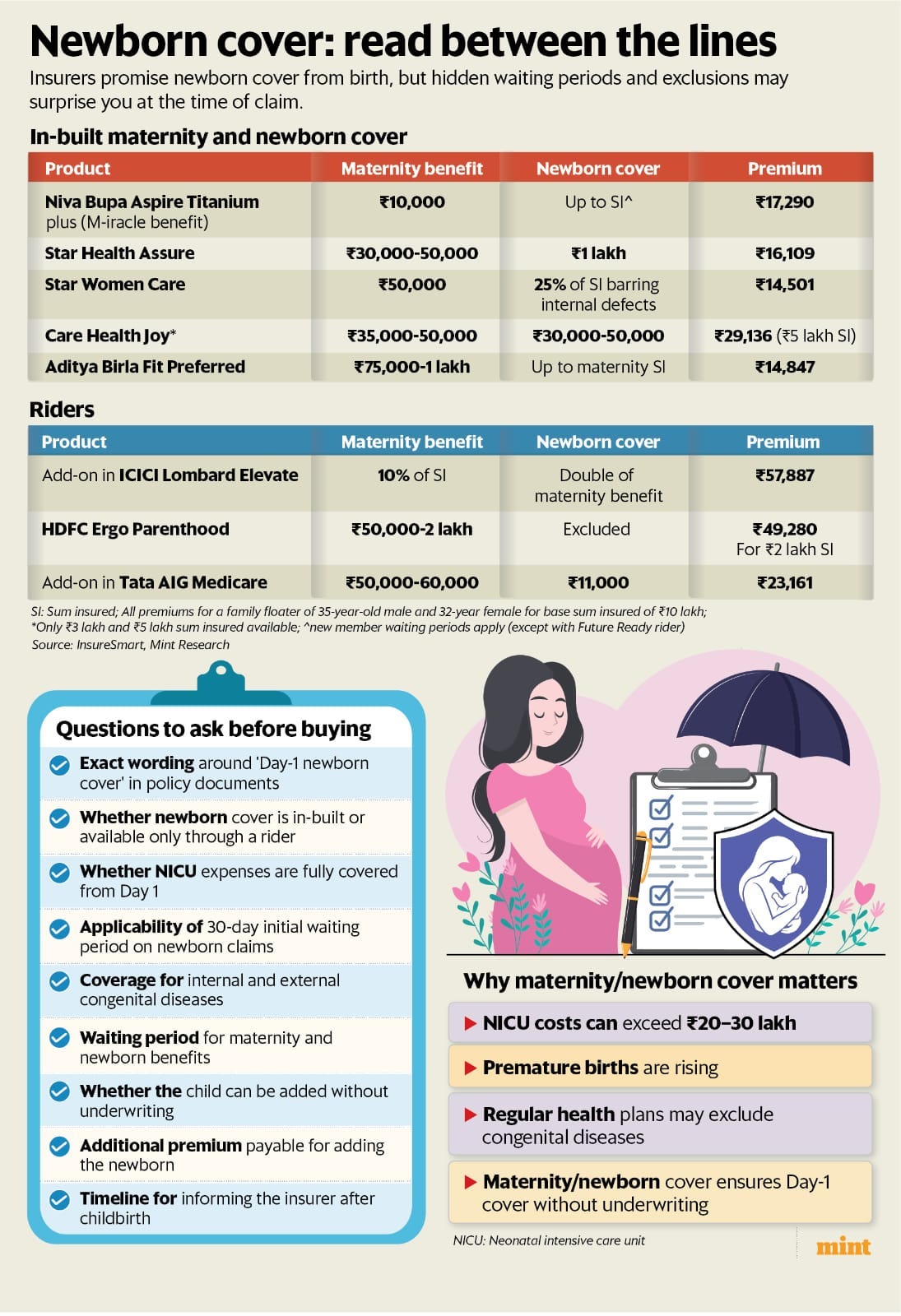

The second story looks at newborn baby covers—an often misunderstood aspect of health insurance. When couples buy a family floater health insurance policy, it doesn’t automatically mean that a child born thereafter is covered from birth. Insurers allow a newborn to be added only after 90 days, and, even then, subject to underwriting. This means a medical condition that the newborn may have could make the child ineligible for insurance.

This is where newborn covers come in. They offer protection from day one, but with a catch: Most come with an initial waiting period of around 30 days, which means the complications at birth may still not be covered. Aprajita Sharma breaks down what parents need to watch out for.

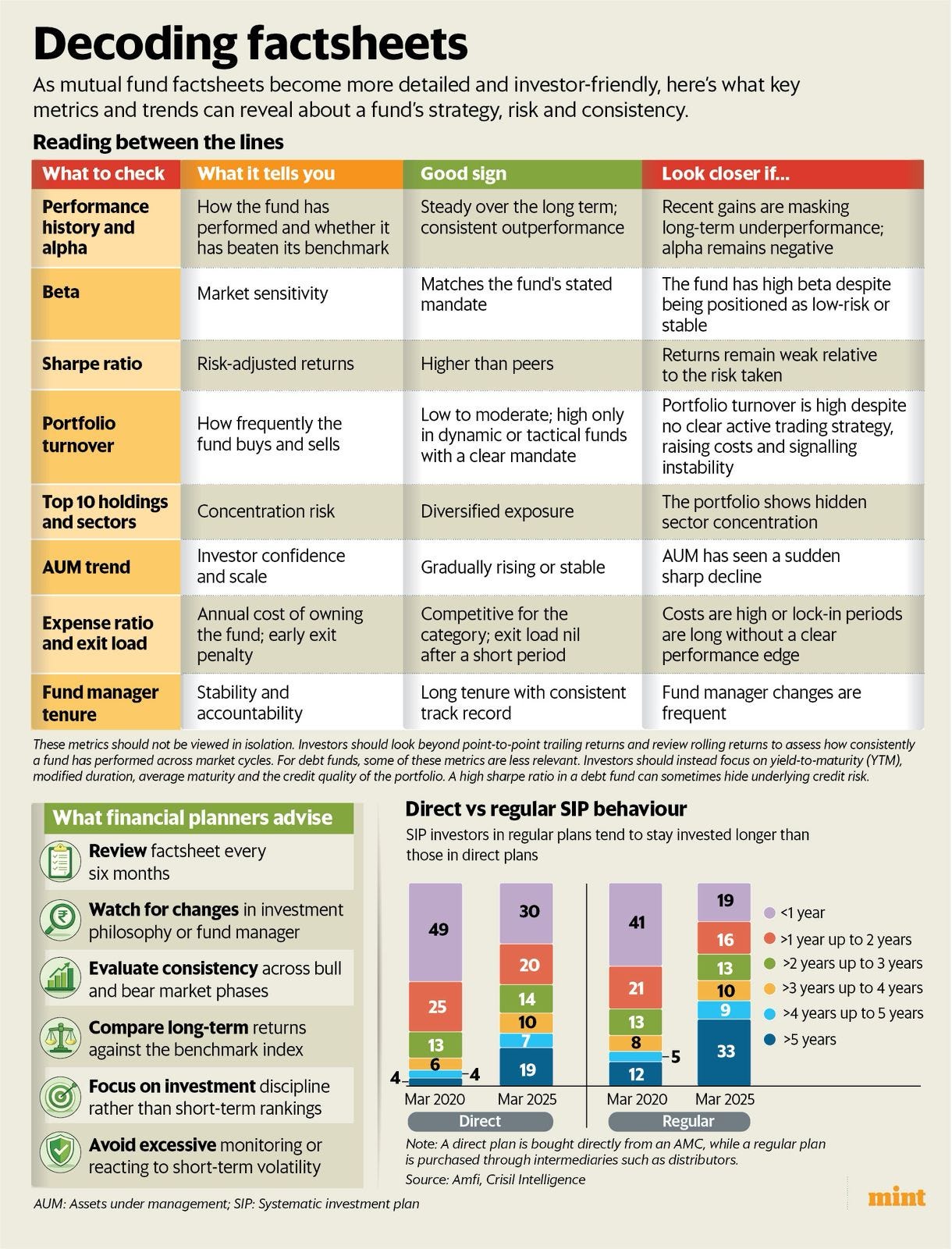

In the investment space, Ananya Grover explores how mutual fund factsheets are evolving from compliance-heavy documents into investor-friendly guides. Fund houses are trying to make their factsheets DIY-friendly by offering clearer insights into portfolio strategy, sector exposure, risks, and fund manager actions. The story also highlights what to look for and the red flags to watch for when reviewing your MF factsheet.

In this week’s Money Guru, Jash Kriplani speaks to Vikas Garg, head of fixed income at Invesco Mutual Fund, on what rising bond yields mean for investors, how to position debt portfolios and why longer-duration funds may present a tactical opportunity in the current environment.

That’s all from the Mint Money team this week. Until next time!

Deepti Bhaskaran is editor, Mint Money, with two decades of experience as a personal finance journalist. Her work reflects a strong focus on financial literacy, consumer protection and practical money management. She can found at deepti.bhaskaran@livemint.com.